Am I gonna win or lose? Sell or hold?

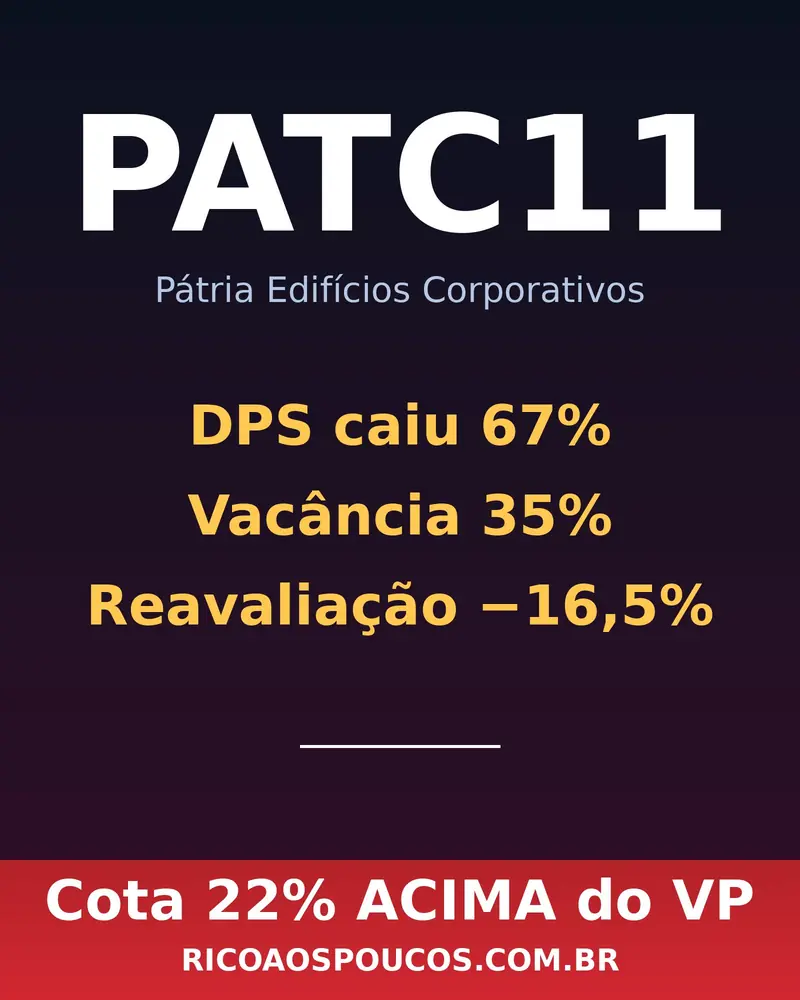

Objective summary for those who have PATC11 or think about buying: the R$ 38,35 (19/05/2026), you pay 1.15x the equity value in a slab FII where the industry average negotiates at 0.80x. The risk of falling is from 13% to 30% only by convergence to multiple pairs — and meanwhile, the dividend of R$0,05/unit yields annualized DY of 1,7%, against CDI of 14,5%.

Has the operation really improved? Yeah. Vacance fell in half, reserve stopped bleeding. But the better. That's it. the price of the unit — and the DPS has been stuck for 10 months, with no sign of rise.

Verdict: AVOID AT THIS PRICE. . Who already has, the case to maintain is weak — it only makes sense for those who bet on the lease of the 1.345 m2 still vacant in Sky Corporate (R$0,05 → R$0,08-0,10) and is willing to accept 12-30% of market marking risk.

(34,7% Dec/25 → 17,3% Apr/26)

(locked in R$0,05 since Jul/2025)

What Really Changed Between December and April

The previous analysis, published in March 2026, painted an ugly picture: physical vacancy of 34,7%, financial 36,2%, payout above 100% burning reserve, DPS already cut three times in 9 months. The April Management Report (doc 1189884, delivered in 13/05/2026) shows a materially different background — on three specific indicators.

Why the DPS didn't go up if the vacancy fell in half

Here's the part that the report doesn't say in all the letters: the fall in vacancy replaces the cashier, no Increases profit. . Full Sales came in paying market rent in the middle of Berrini today, not in pre-2020 levels. And the asset, remember, was acquired on a higher rental cycle.

In other words, the country-VBI management executed well what it had to perform — it closed the easy half of the vacancy (the part where the target rent is compatible with the current market). The other half depends on the office market in Berrini to reheat or aggressively discount the m2. The fund chose to hold price.

The timeline of the dividend that does not forget

Whoever bought PATC11 before Jun/2025 saw the DPS drop 83% in three consecutive cuts. Whoever bought it after Jul/2025 is living 10 months of R$0,05 — enough to become normal.

The portfolio in 4 assets — 1 concentrated problem

Three of the four assets are 100% leased. The problem is that the fourth — the largest — concentrates 38% of the estate and still has half of the vacant area. It is not diversification that is lacking: it is resolution of a specific asset that weighs.

The elephant in the room: P/VP 1.15x in a sector at 0.80x

Here's the only thing that matters to anyone who thinks about buying now. PATC11 negotiates R$ 38,35 with equity value of R$ 34,31 — a 12,7% prize in relation to the book itself. In the corporate slabs sector, the average IFIX-Office negotiates at 0.80x VP. PVBI11 It's at 0.87x. RCRB11 in 0.78x. VINO11 under 0.70x. XPCM11 He's got a weaker case and he's negotiating less than half a book.

The argument for the award would need to be robust: exceptional management, irreplicable premium assets, clear recycling pipeline. The VBI country has executed the recent turnaround well, yes — but the portfolio is reasonable, not iconic, and there is no catalyst advertised to change the thesis.

Three scenarios for the unitholder to think coldly

And on the unit, what can happen?

Where are the unit 1.700s that came out

From January 2025 to March 2026, PATC11 lost 28% from the unit base — from about 6.100 to 4.407. This flow does not happen in the background with clear thesis and growing PSD. It happens in background whose unit went in waiting for R$0,15/month, saw the dividend drop 67% and realized that management chose to hold rental price instead of speeding up the lease.

The good news is that this base adjustment has probably gone through the worst. The bad news is that what is left tends to be heavy unit, positioned, and that will sell if it appears 5-10% of unit improvement — limiting upside in the short term.

PATC11 is not a bad FII. It's an FII. expensive, in a sector where the 20-30% discount on VP is the rule. Paying 1.15x VP for an operational improvement that still needs to turn dividend is to fund the fund manager's turnaround with his own pocket — and the 10 month history of stopped DPS shows exactly how much management is willing to share this upside with you.

Sources, validation and disclaimer

Basic document: Apr/2026 (Doc. 1189884, delivered 13/05/2026).

Independent validation: Cross indicators with Status Invest and Funds Explorer in 19/05/2026 (DPS R$0,05, physical vacancy 17,3%, P/VP 1.15x).

Quotation used: R$ 38,35 in 19/05/2026 (base date of analysis).

Disclaimer: Informational and analytical content — does not constitute a recommendation for the purchase, sale or maintenance of assets. Past dividends do not guarantee future dividends. Evaluate your risk tolerance before investing. Background: Country Corporate Buildings FII (CNPJ 35.652.078/0001-50), Country management-VBI, BTG Administration Practical.