3 shocks overlapped in hours

It's not a real estate crisis. It is the reflection of NTN-B long paying ~7% real sovereign risk — while it exists, the average investor prefers Treasury to Brick FII. Five vectors compress IFIX for the same reason.

5 vectors compressing IFIX at the same time

Even good fund manager falls when the backdrop tightens. It's not a microscope — it's the macro:

Selic — Silent Guillotine

NTN-B long paid ~7% real sovereign risk. Brick FII needs to deliver 9-10% to compete — or the unit drops. The adjustment takes place by unitNot for the rent.

IPCA leans on the ceiling (4,5%)

Inflation scraping the limit ties the Copom. Worse: April relief came from gasoline — when the R$ 5 dollar passed on to imported derivatives, the IPCA returns with 2-4 months of lag.

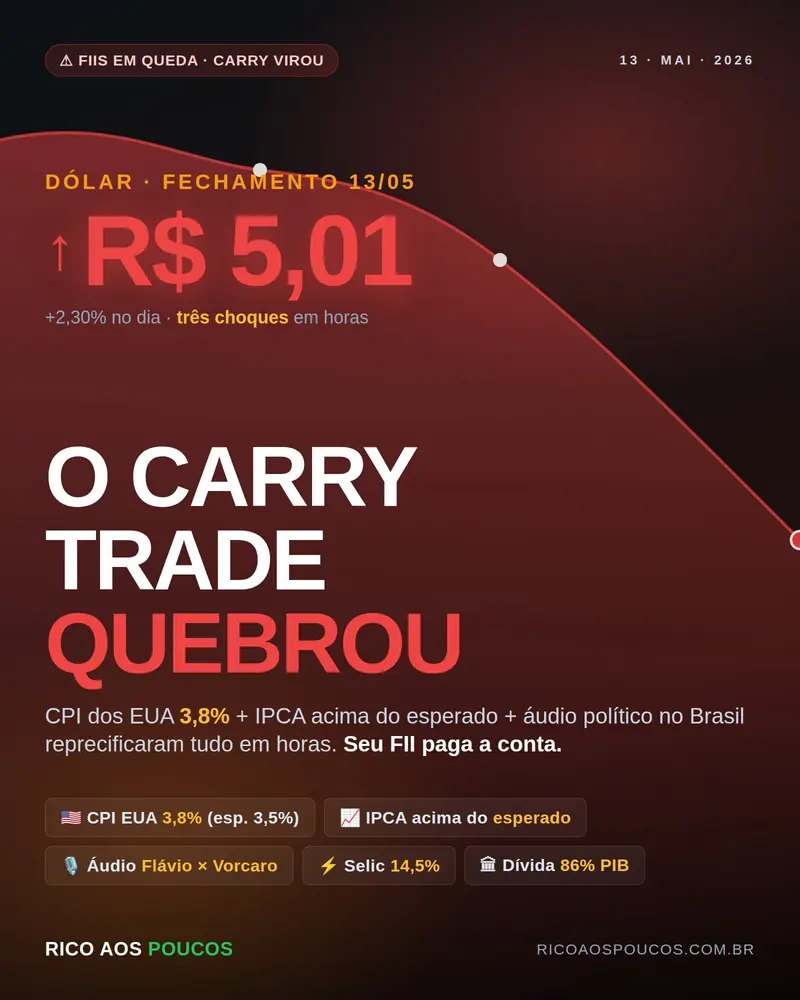

Carry trade closing

Cheap jan-abril dollar was artificial — foreign flow of 61,2% from B3 overturned the exchange by carry. Exogenous shock today closed the trade in hours. YTD data is a photo of the past.

Debt/GDP charging toll

Of ~72% (end 2022) for projection of 84-86% (end 2026). Market charges prize in NTN-B long — exactly the asset that serves as mirror for FII brick. Interest paid by the Union: ~R$ 1 trillion/year.

Election reprecises real-time risk

Research swings IFIX in weekly waves. The foreign flow reprecises implicit probability of each scenario — today's audio Flávio × Vorcaro is the cleanest example of this mechanism.

Live case: the audio that re-enacted everything in hours

Market had been pricing exchange for "market-friendly" application (seen as more predictable on the fiscal tip) with non-trivial probability. Any event that reduces this implied probability increases the risk premium — and IFIX, sensitive to long NTN-B, pays more than proportionally. "More favorable to the market" is not judgment on which government is best for the country; it is technical reading. Noun political analysis remains for the reader.

Why High Yield (CACR11, VGHF11) falls more than blue chip brick

Everything we've listed so far affects the entire IFIX — but it affects unevenly. . The most bleeding FIIs in May/2026 have a common profile: high-yield paper with exposure to incorporation or multiproperty CRIs. . Why:

| Vector | How It Affects Blue Chip Brick FII (KNRI11, HGRU11, VISC11) | How It Affects High Yield Paper FII (CACR11, VGHF11, HCTR11) |

|---|---|---|

| Selic 14,5% | Quota falls for arbitration with NTN-B, but rent keeps entering | CDI high debt suffocation (CDI+spread becomes priceless) — defaults appear |

| IPCA leaning against the ceiling | Rent adjustment helps in the short term | In CRI of construction, construction cost goes up together and burst schedule |

| Cheap Dollar | Neutral | Embed imported input (steel, glass, finish) — when turning back strong |

| Debt in 86% GDP | NTN-B high flat rate | Private credit suffers more than public — investor requires larger spread |

| Election | Cyclical volatility | Institutional flow comes out first than is less liquid |

| Result in May/2026 | 5-12% drop in the year | 17-60% drop in 12 months |

It's no coincidence that the CACR11 accumulates near 60% drop in 12 months and the VGHF11 mark something around 17% only in May (externally consulted quotations — the site's own tracker is still in stabilization and the numbers should be checked in the Status Invest / Funds Explorer before any decision). These are funds that carry embedded credit risk. — and in an environment of prolonged high interest rates, this risk appears as default of CRI, work delay, suspension of dividend. The unitholder bought DY from 19% thinking it was income; what he bought was credit risk premiumAnd that award is now being charged.

Who is in well-placed brick bottom (corporate slab A+, dominant mall, logistics shed in São Paulo) is seeing fall uncomfortableBut the rent hasn't stopped dripping. Who's on high yield is seeing fall structural, with real risk of zero dividend for months.

5 marks for the fall to stop

Selic below 12%

Cutting cycle continuity — not enough -0,25 single April pp.

IPCA retreating from the ceiling

For ~3,5-4%. It depends on fuel, food and dollar not to fire.

Consolidated electoral research

Anywhere. Prolonged uncertainty penalizes more than result.

Balanced dollar

Medium-term between artificial R$ 4,89 and current exchange stress.

Clear tax signal

Primary surplus delivered, respected framework, long interest yielding.

.Metric-summary to accompany: NTN-B 2035 below real 6,5%. . Today is above 7%. Each 0,1 drop point is direct relief to the price of brick FIIs.

The equation of the day

The three of us together do not add up — multiply. . This is how the trend turns: structural precondition finding specific catalyst.

The uncomfortable truth: FII's unit in 2026 bought a derivative of NTN-B without knowing that. . As long as Selic stays in 14,5% and long interest charge real 7%, the shed may be 100% rented, the mall may be crowded, the rent may be readjusted by IPCA — and yet the unit will fall. It's not the fund manager who made a mistake. He's the one who bought it thinking it was "passive income guaranteed" and in real bought risk of duration that he can't measure.

May/2026 is the beginning of re-enactment, not the end. There is still an investor queue entering FII IPO thinking 12% DY is guaranteed. When this queue understands that it bought long-term risk packaged from "immobile", the discount will be much higher than today's.