Current photo: May/2026

The full numbers

What is VRTM11 — in a wallet

O VRTM11 It's the Factor Verità Multistrategy FII, Fund of the Bank Factor managed by the FAR (Resources Management Factor). The proposal is to give it to the unit holder, in a single ticker, multi-category diversified exposure — controlled mix of developing real estate, real estate credit and listed FIIs, with active rotating management between the three classes. The current composition:

IPCA+11% a.a. + kicker 2-5%

IPCA+10% / CDI+3,5%

diversified (in reduction)

ZQX0ZX mi in RF

In absolute numbers: 90+ active, HHI of 0,024 (very sprayed), top-10 covering only 28% of PL and top-1 (CRI Fiber) representing 6,82%. Yeah. actual spray — undeclared — and acts as a buffer against a specific event (default of a CRI, vacancy of a property, maturity of a contract). That's the best structural catalyst on the bottom.

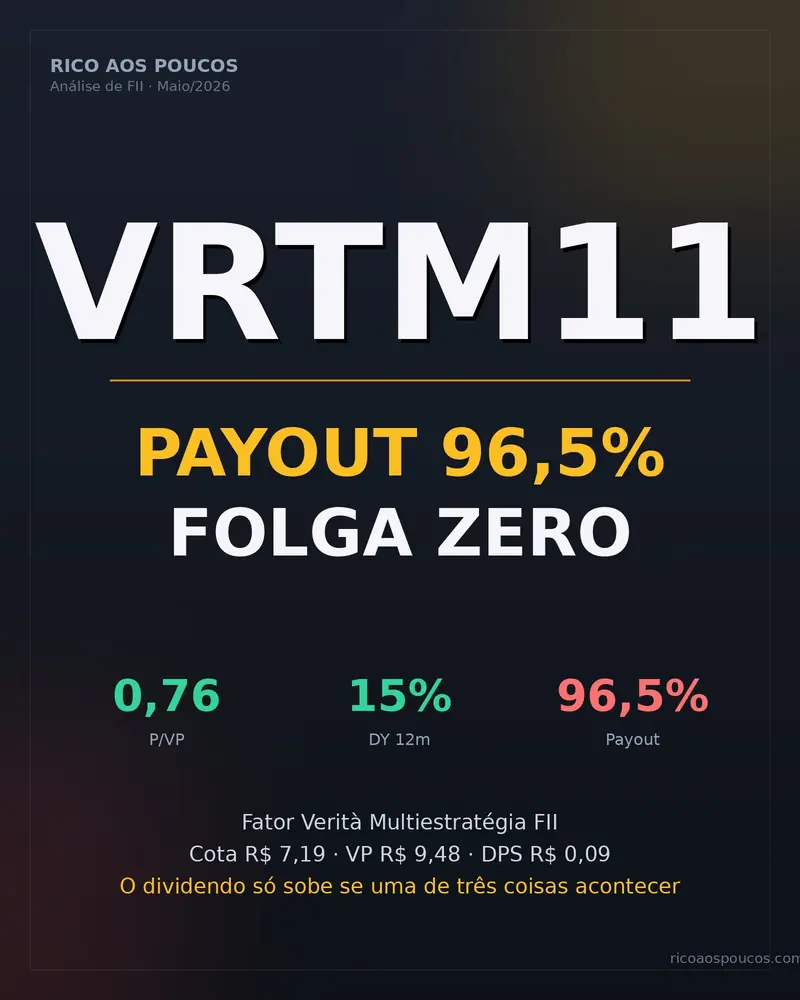

Why the payout in 96,5% is the blind spot

The account that defines the dividend

Cash result for the last 12 months: R$ 51,85 million. . Distributed over the same period: R$ 50,02 million. . O 96,5% payout It means that the fund gives the unit practically everything it generates. The calculated sustainable DPS is in R$ 0,092/unit — exactly in line with the R$ 0,090/unit which the fund has been paying for 18 months without oscillation.

In funds with 80-85% payout, there is room for extraordinary distribution at the end of the semester, to cushion a bad month of coupon or to support the DPS when the IPCA falls. There isn't any here. Every extra penny that the unit holder wants to see in the DPS needs to come from one of the following three levers — there is no reserve of expressive result or operational slack to "stretch" the dividend organically.

The only 3 levers for DPS to grow

For the fund to earn more without adding more, the fund manager needs to find an asset whose internal return rate beats net 11% (above the current portfolio delivers on average). It's hard in the heated market — what the fund manager said he was looking for now is precisely this: CRIs mid-yield and new residential properties with target return IPCA+10 to 12%.

Trigger: pipeline FARBuildings in development have a repurchase clause by the builder at the end of the work. If the buyback happens above the disbursed by the fund, the extra gain (the kicker) enters the result box. The estimated potential is up to R$ 0,078/unit per event — almost a monthly DPS. But it depends on the delivery of the works, the regional real estate market and the builder's willingness to exercise the option.

Trigger: delivery of workThe fund manager stated that he is reducing the share in listed FIIs — sales already made in 2025 include positions in BRCO11, ZAGH11, OULG11, KNSC11, MCCI11, JSRE11 and OUJP11 — some to the detriment (R$ 2,99 mi non-recurring negatives). For this rotation to help in the DPS, the next sales need to come out above the purchase price. Otherwise, the result box falls together.

Trigger: FIIs cycleThe elephant of negative reassessments in 2025

The Annual Report 2025 listed seven properties with negative revaluation material in the portfolio of developing enterprises. In percentage values:

Most of these markings are MTM assets in assets still in work — it is not cash that came out, it is fair value that has been adjusted down. The optimistic reading is that, with the delivery of the work and the repurchase above the disbursed (the kicker), part of that loss may reverse accountingly. . The realistic reading is that the execution risk is real: the longer the schedule delay or the worse the regional real estate market at the time of delivery, the less chance the builder will exercise the buyback or the asset will be sold at an attractive price.

The important thing to note: the VP of R$ 9,48 already contains these negative reassessments. . The unitholder who enters today R$ 7,19 is paying 76% on an equity value that has already incorporated this discount. It is a double discount — market price below VP, and VP marked with embedded losses.

Performance Rate: 20% over IPCA + IMA-B 5

O VRTM11 charges the unit holder a 20% performance rate on what the result exceeds the IPCA + Yield IMA-B benchmark 5. The fee is provided daily and paid every six months (June/December). In positive cycles for the fund — when there is repurchase of units, relevant patrimonial valuation or closing of macro favorable spread — performance takes part of the upside of the unit holder. In 2025, the amount paid was 0,20% of the accounting PL (0,25% at market value).

It's a number that looks small, but in high cycles it turns drag. For comparison, "traditional" brick backgrounds like HGRU11 or KNRI11 do not charge performance — only administration. Those who enter the VRTM11 are paying for the "active multi-category management" thesis, and performance is the counterpart of it.

Low liquidity limits position

R$ 257 thousand/day, in practice

The mean daily volume of VRTM11 in the last 30 days is R$ 257 thousand (Status Invest confirms R$ 263 thousand on 15/05). Applying the consensual 20% ceiling of daily volume to enter or exit without moving price, a position of R$ 500 thousand takes about 10 business days. R$ 1 million It takes almost 20 days.

This eliminates the fund from the list of candidates for institutional investor or for large retail portfolio. For the private investor with R$ 50-100k positioned, liquidity is reasonable — but it is worth remembering that in times of market stress, liquidity always gets worse, and lower liquidity funds tend to suffer additional discounts.

Who VRTM11 is for

| Makes sense if you're... | It doesn't make sense if you... |

|---|---|

| Investor who wants 1 ticker as a multi-category sub-cartel — you do not need to mount 10+ separate FIIs to diversify. | Search Growing DPS. . Payout 96,5% leaves zero structural slack — the dividend only rises via specific event. |

| Take it. indirect exposure to residential buildings in development, with the risk of execution of work. | You need to high liquidity. . ZQX0ZX thousand/day limits positions above ZQX1ZXk. |

| Yes. satellite position (≤5% of the FII portfolio) betting on convergence of P/VP 0,76 → ~0,90. | He's retired looking for predictable monthly income with zero risk. . Multistrategy is by definition more volatile than pure brick. |

| Valuing actual spray (HHI 0,024, 90+ assets, top-1 = 6,82%). | Yes. pure sectorial exposure (logistics, paper, shopping) — multicategory dilutes the thesis. |

| Checks to monitor quarterly the kicker execution (repurchases) and the evolution of works. | Rejects performance rate. . VRTM11 snake 20% over IPCA + IMA-B 5. |

. Analytical Verdict — KEEP (Note 7,0)

O VRTM11 It's a fund. technically well-built: actual spray, active rotating management, three classes of assets under one vehicle, residual repo (kicker) as optional upside. The R$ 7,19 (P/VP 0,76), the discount on the VP marked with work losses is factual — who enters today pays a unit that has already recognized much of the negative MTM.

But structural fragility is the 96,5% payout. . Without a significant reserve, the R$ 0,09 DPS only goes up via three levers — premium acquisition, exercise kicker or positive rotation on listed FIIs —, and two of them depend on execution. Those who come in waiting for "growing division of multi-category FII" are buying a thesis that is not on the balance sheet.

To whom There's already a unit., the reading is keep: the double discount thesis remains, and the actual source of upside is in the next 12-24 months of repo execution. To whom There's no unit and multi-category search with more traction of DPS, it is worth comparing with more mature pairs — brick backgrounds + paper with payout in 85-90% have more slack to sustain and grow the dividend, even without the angle of real estate kicker.

The statement that needs to be said

VRTM11 is not a cheap FII. It's a correctly priced IFI for those who understand what they're buying. The P/VP 0,76 and the DY of 15% are not market distortions expecting convergence — they are the price that the market pays for a portfolio whose VP has already been bitten for negative reassessments, whose 96,5% payout holds the DPS at the current level and whose only growth lever requires three specific events (premium acquisition, kicker and profitable FII sale) to deliver in sequence and in scale. Who buys R$ 7,19 thinking they're paying 76% from a "clean" equity is looking at the wrong number — the relevant equity already has the embedded discount. And who buys by "dividing increasing multi-category fund" is confusing the active management thesis with coupon payment management — these are different things, and the VRTM11 delivers the first, not the second.